I woke up this morning to a notification that nearly made me spit out my green smoothie.

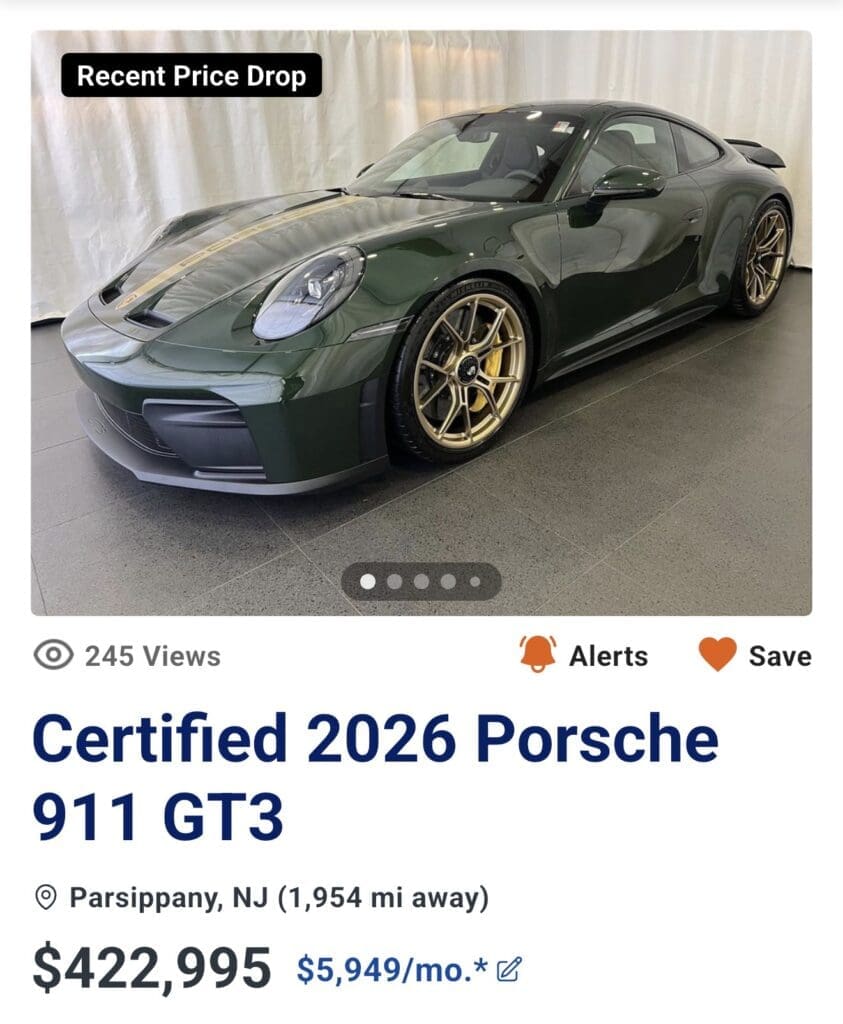

“The Porsche you’re looking at just dropped in price. Now only $422,995.”

I laughed out loud. Bargain of the century, right? Honestly, let’s buy three.

Here’s the backstory. When my husband and I bought our place in Utah, we needed a four-wheel-drive vehicle for the snow. I ended up with a Tesla Y, which I love so much I genuinely don’t think I’ll ever own another car that isn’t a Tesla.

But while we were shopping around, I logged into my husband’s car-search account to compare options.

I forgot to log out.

So now I get notifications about every Porsche he’s ever clicked on. Including this one — half a million dollars, with a casual monthly payment of $5,949.

Five thousand, nine hundred and forty-nine dollars. A month.

And that notification got me thinking about something I see entrepreneurs do every December.

You know the advice. Your CPA calls you in late November and says something like, “You had a great year. You’re going to owe a lot in taxes. You should buy a vehicle before December 31st to reduce your liability.”

On paper, that sounds smart. Section 179 deduction. Bonus depreciation. Lower tax bill.

So the entrepreneur goes out and buys a $90,000 SUV. Or worse — a Porsche.

Here’s what nobody talks about.

That tax write-off is only worth a percentage of the purchase. If you’re in a 30% tax bracket, you saved $27,000 on taxes. Cool. But you also just inherited a $1,500-a-month payment (or in this case, a $5,949-a-month payment) for the next five to seven years.

You didn’t save money. You spent $90,000 to save $27,000.

And now your business has a giant fixed expense that doesn’t bring in a single dollar of revenue.

That’s not tax strategy. That’s emotional shopping wearing a suit.

Here’s the rule I want you to write down somewhere.

Before you buy anything to “save on taxes,” ask yourself one question:

Will this purchase generate revenue, or am I just buying it to feel productive?

A piece of equipment that lets you serve more clients? Probably worth it. New software that automates a 10-hour-a-week task? Probably worth it. A Porsche that makes your driveway look impressive? Not a tax strategy. A lifestyle decision dressed up as one.

This is exactly what the Profit Planner Method™ is built to fix.

We organize your cash around the things that actually move the needle — not whatever your CPA suggests in a panic on December 28th. Every dollar in your business has a job. And the job of a tax-deductible expense should be to create more revenue, not just shrink a tax bill.

I know there’s a whole genre of business advice that focuses on cutting your $7 lattes. Maybe that matters a little. But the lattes aren’t what’s keeping you stuck.

It’s the $5,949 monthly payments dressed up as tax savings.

It’s the equipment you bought because someone told you to, not because you needed it.

It’s the investments that don’t generate revenue but feel productive in the moment.

Without a system, every December turns into a panicked shopping spree.

With one, you make calm, profit-first decisions all year long.

If your business made revenue this year but you’re not sure how much of it is actual profit — and you’re definitely not sure what to do about taxes — come spend an hour with me.

The free Business Finance for Women Master Class walks through the whole thing. How the Profit Planner Method™ works. Why most “tax saving” advice costs you more than it saves. And the system that lets you keep more of what you make without buying a Porsche to do it.

Save your seat for the Master Class

Otherwise, you don’t have a business. You have an expensive job.

|

P.S. — My husband, for the record, has not bought the Porsche. (Yet.) But every time that notification pops up, I’m reminded how easy it is to talk yourself into a “deal” that’s actually a 60-month commitment. Your business deserves better math than that.